While property professionals and investors have become more aware of the concept ‘risk’, they often struggle to truly understand its meaning and the potential impact on their financials.

The major financial risks associated with purchasing a property are:

- Equity Risk;

- Cash Flow Risk; and

- Settlement Risk.

Equity Risk

Equity risk is the risk that the property price may reduce, or the property may deliver poor capital growth. The reasons for that are: the location of the property; the type, configuration and the quality of the property, and the holding period of the property (typically the shorter the period, the higher the risk of a short-term loses).

We often hear that ‘there isn’t any impact, as eventually, in 10 years this property will deliver a good capital growth’. This is a common mistake. The overall capital growth of a property carrying low risk delivering solid capital growth, is significantly higher than a property that carrying higher risk delivering low capital growth.

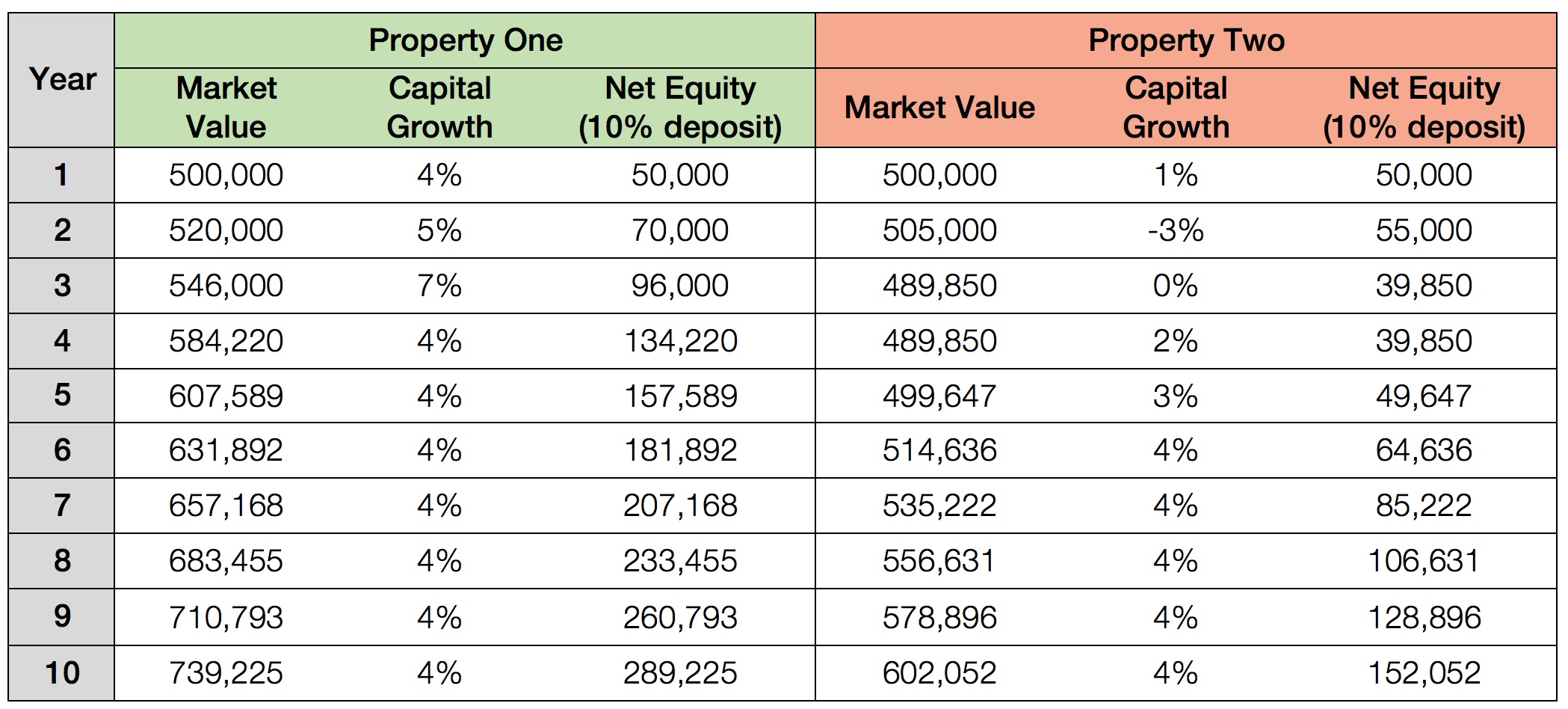

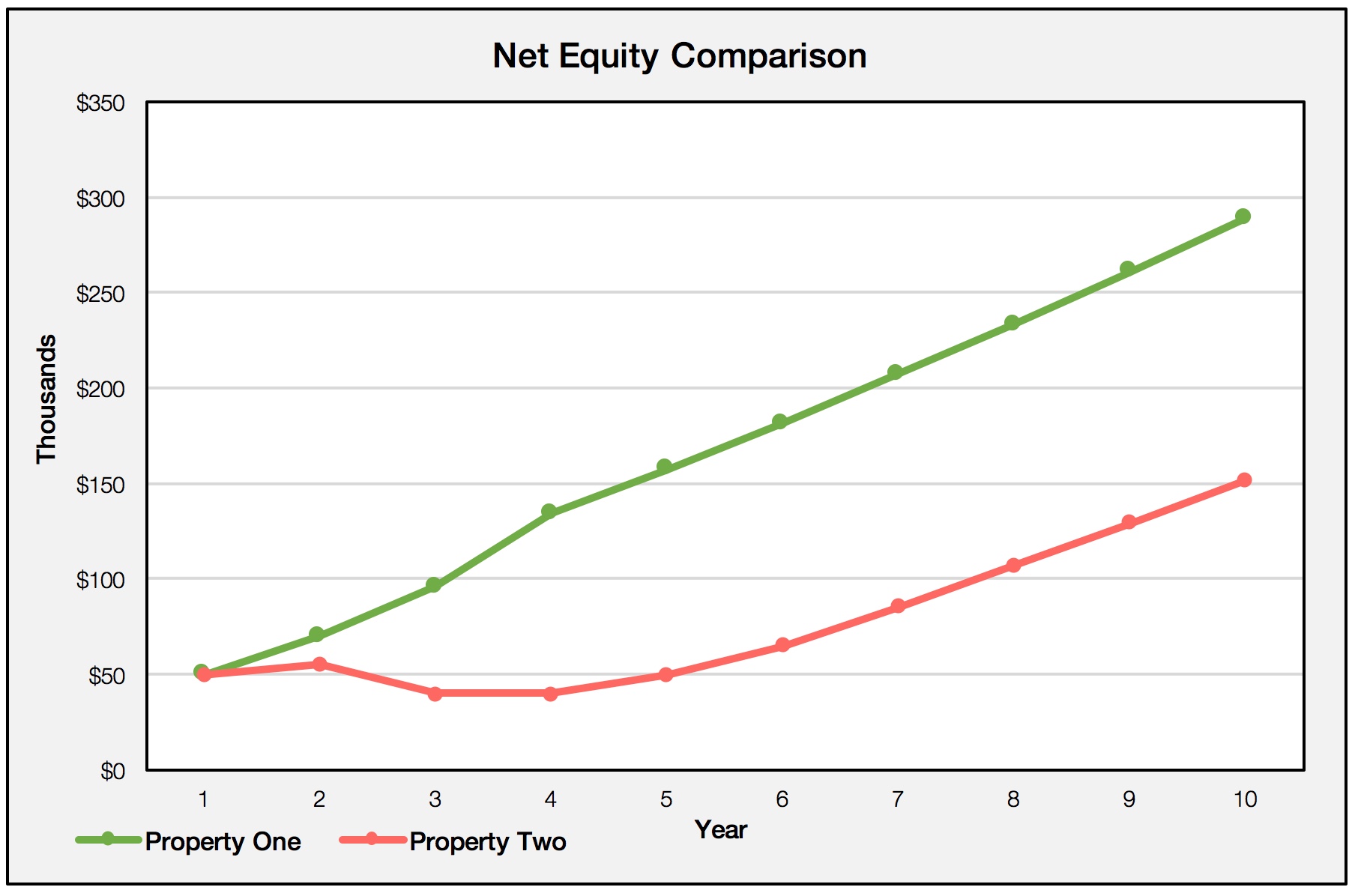

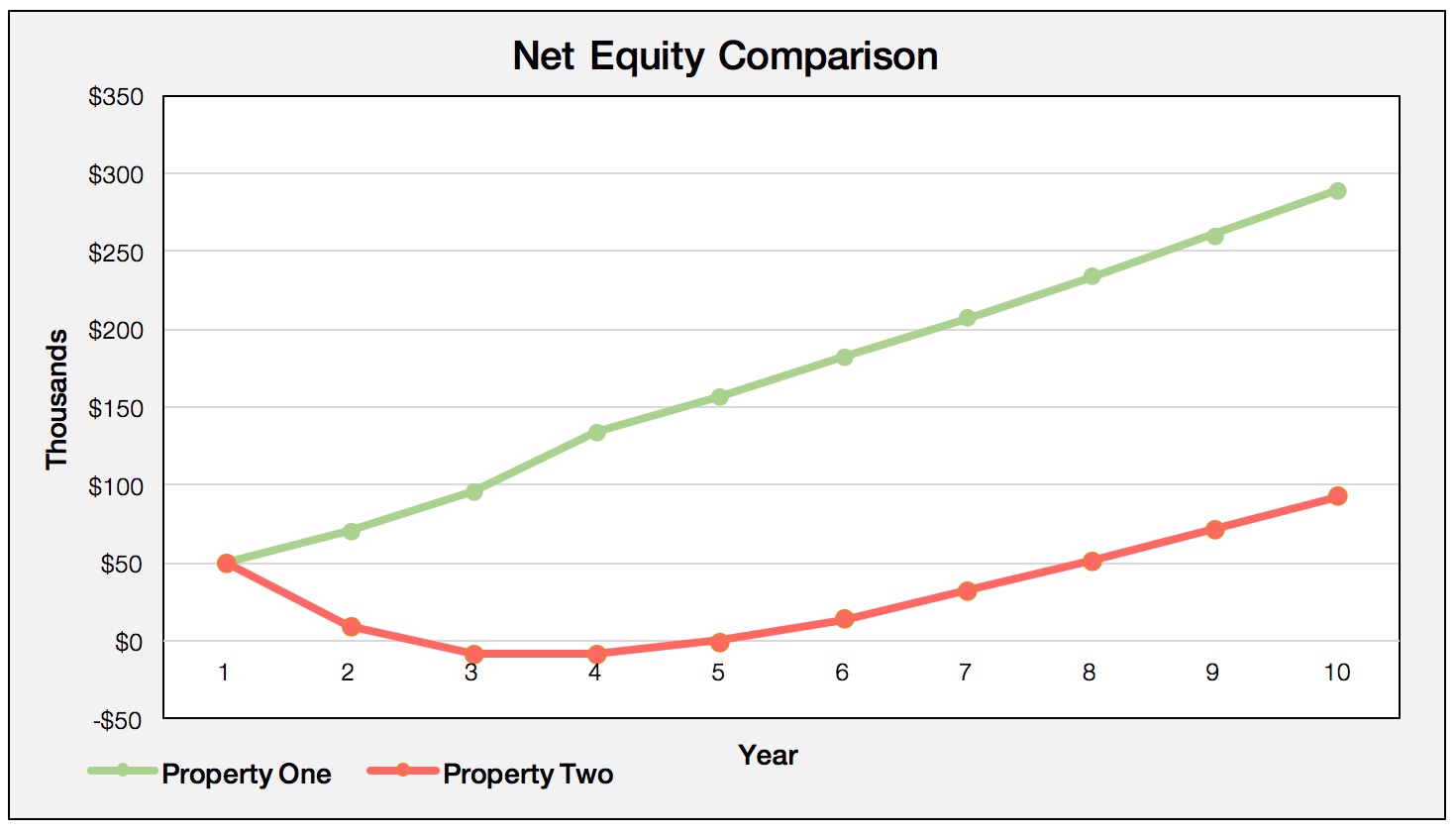

Let’s compare two properties. The first carries low risk and delivers consistently good capital growth. The other delivers poor capital growth only in the first few years.

While the market value of these properties was identical, after 5 years the gap was 23%, reflecting a price difference of more than $100,000. Even if, from year 6, the capital growth (in %) was the same for both properties, after 10 years, the gap would still be approximately $140,000. This gap is, effectively irreversible, and will only increase in the following years.

Overall, the net equity of property one is about twice as the net equity of property two (under the assumption of a 10% deposit)

Cash Flow Risk

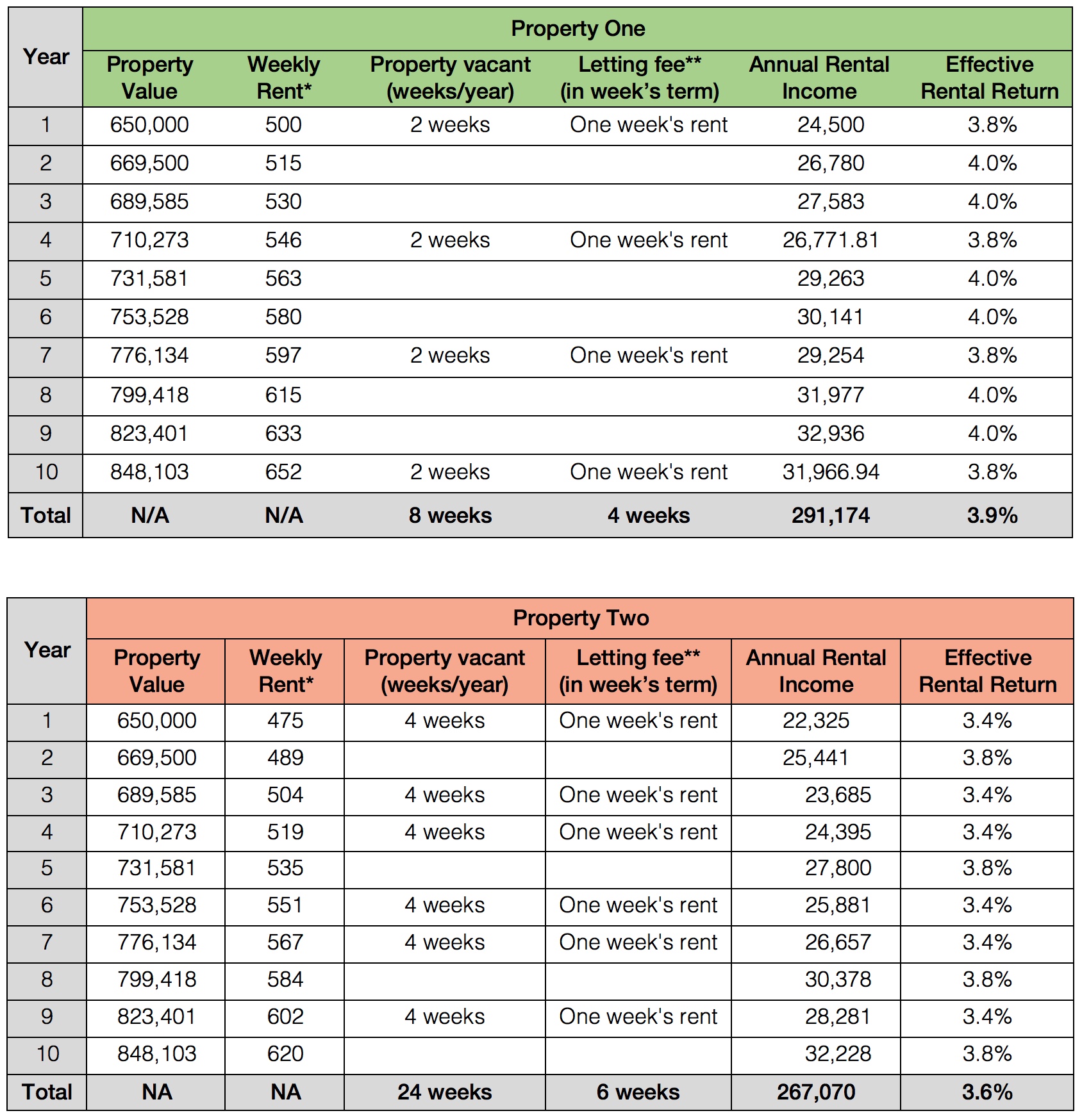

The actual rental return may be poor and the landlord must therefore cover the shortfall between the rental income and the ongoing costs.

Put simply, properties carrying low cash flow risk are highly competitive among tenants, and are therefore unlikely to remain vacant for long periods of time. On top of that, tenants tend to stay in these properties for longer periods of time, subsequently reducing the costs associated with the property. These costs include ‘letting fees’ and other small improvements that are often needed when a property is up for rent.

To demonstrate, let’s compare two properties, both with identical market value. However, one carries low cash flow risk, appeals to a large audience, and delivers 4% gross annual growth. The other carries medium risk, as it appeals to a smaller audience and therefore delivers 3.8% rental return. It also takes a longer period to find tenants for that property and they tend to stay for shorter periods of time.

Settlement Risk (for Off-the-Plan Properties)

Settlement risk is the risk that the value of the property prior to the settlement will be lower than the ‘formal’ property value in the contract. According to recent research, the valuation of around 50% of units is some areas is lower than the contract value. This results in a shortfall between the valuation and the property price, which needs to be covered by the buyer.

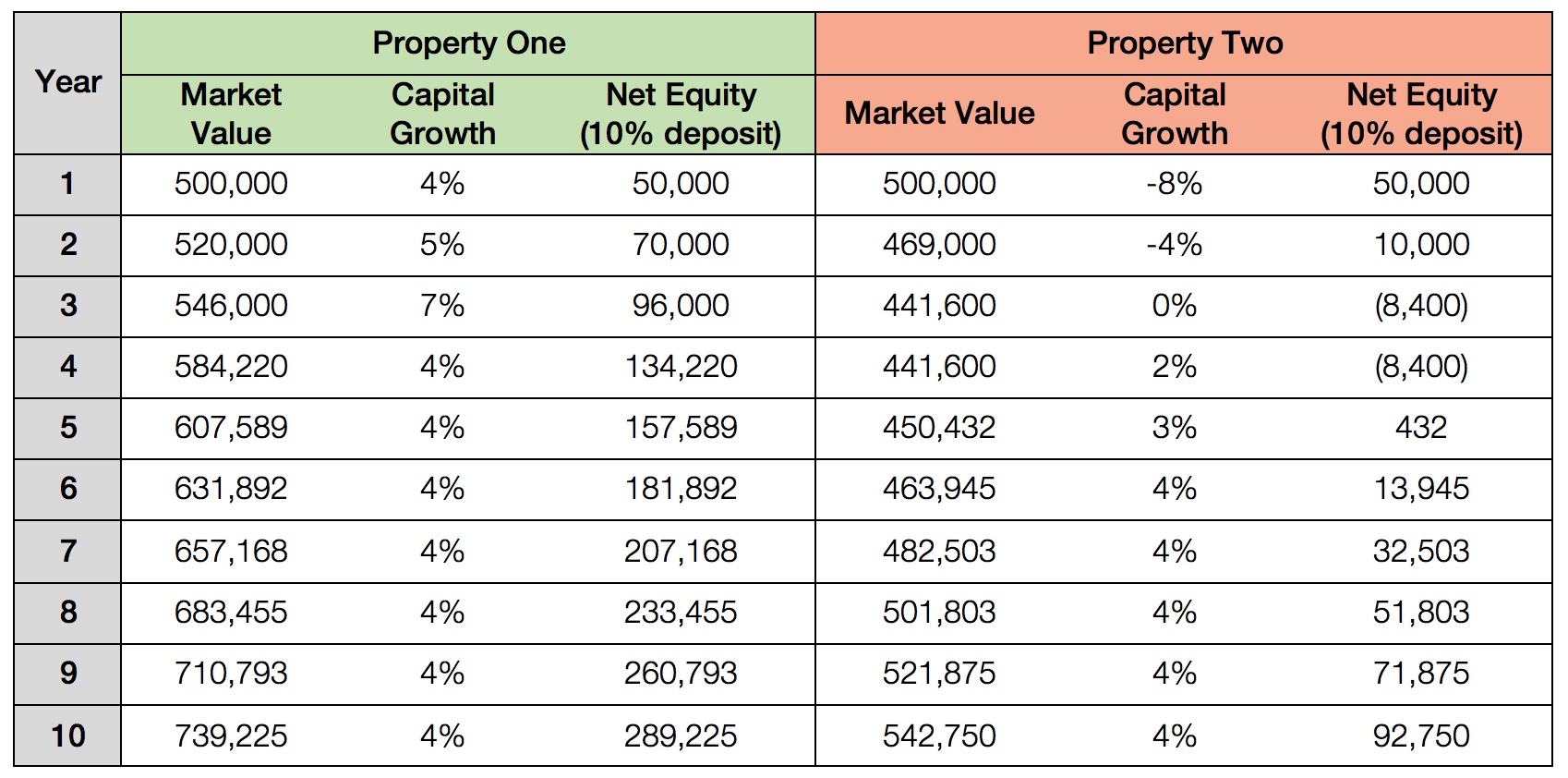

The numerical example is similar to the one that relates to equity risk, with one major difference – the losses can be significantly higher.

Overall, the net equity of property one is about three times as the net equity of property two (under the assumption of 10% deposit).

Overall, the net equity of property one is about three times as the net equity of property two (under the assumption of 10% deposit).

Our custom-made reports are available thorough: RiskWise Property Review